What’s Driving 5.9% CAGR Growth in Metal Anticorrosion Additives Market?

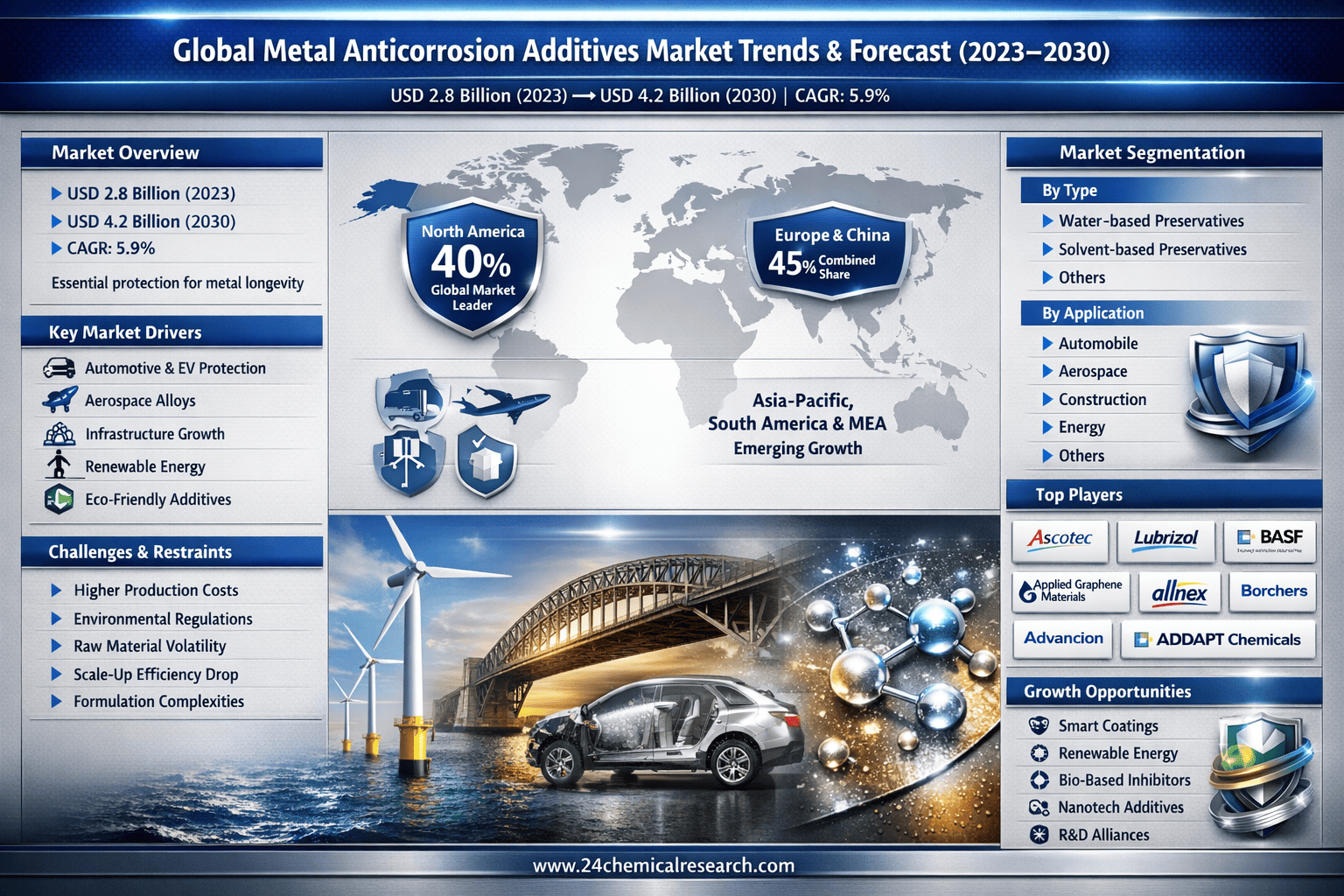

According to 24Chemical Research, Global Metal Anticorrosion Additives market was valued at USD 2.8 billion in 2023 and is projected to reach USD 4.2 billion by 2030, exhibiting a remarkable CAGR of 5.9% during the forecast period.

Metal anticorrosion additives, essential chemical compounds designed to inhibit the degradation of metallic surfaces caused by environmental factors, have transitioned from specialized formulations in industrial settings to vital components in modern manufacturing. These additives, often integrated into paints, coatings, and lubricants, provide a protective barrier against oxidation, moisture, and chemical exposure. Their key attributes—such as enhanced adhesion, long-term durability, and compatibility with various substrates—position them as indispensable for prolonging the lifespan of metal structures. Unlike traditional rust preventatives, contemporary metal anticorrosion additives emphasize eco-friendly compositions, enabling seamless incorporation into water-based systems and aligning with global sustainability goals.

Get Full Report Here: https://www.24chemicalresearch.com/reports/262952/global-metal-anticorrosion-additives-forecast-market-2024-2030-56

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

-

Surge in Automotive and Aerospace Demands: The incorporation of metal anticorrosion additives into vehicle coatings and aircraft components stands as the primary growth engine. The automotive sector, a global powerhouse valued at over $3 trillion, constantly seeks materials that enhance fuel efficiency and reduce maintenance costs through superior corrosion resistance. These additives enable the development of lightweight alloys that withstand harsh conditions, potentially extending part life by 25-40% and supporting the shift toward electric vehicles where battery casings require robust protection. In aerospace, where safety is paramount, anticorrosion solutions have shown to minimize galvanic corrosion in aluminum structures, a critical factor in extending service intervals and cutting operational expenses.

-

Infrastructure and Construction Boom: With urbanization accelerating worldwide, the construction industry is fueling demand for durable metal protections. Bridges, pipelines, and buildings exposed to weather extremes rely on these additives to prevent structural failures, which cost economies billions annually in repairs. Modern formulations offer self-healing properties that repair micro-damage autonomously, improving longevity by up to 50% in marine environments. As governments invest in resilient infrastructure—think of major projects in Asia and the Middle East—these additives become key to sustainable development, reducing the environmental footprint of frequent reconstructions.

-

Advancements in Green Chemistry: The push toward environmentally compliant materials is transforming the additives landscape. Traditional chromate-based inhibitors face bans due to toxicity, paving the way for bio-based and nanotechnology-enhanced alternatives that provide equivalent or superior performance without health risks. These innovations, such as silane-based additives, boost corrosion resistance in steel by forming dense protective layers, driving adoption in oil and gas pipelines where failure can lead to catastrophic leaks. The global shift to low-VOC coatings, mandated in regions like the EU, underscores how these drivers align with regulatory pressures while opening doors for cost-effective, high-performance solutions.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/262952/global-metal-anticorrosion-additives-forecast-market-2024-2030-56

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption.

-

Elevated Costs and Formulation Complexities: Developing high-performance metal anticorrosion additives requires advanced synthesis techniques, like organometallic chemistry and polymer encapsulation, which demand precise control and specialized facilities. This results in production expenses 15-30% higher than basic inhibitors, straining budgets in price-sensitive sectors such as consumer goods manufacturing. Moreover, achieving uniform dispersion in coatings remains tricky, with inconsistencies leading to patchy protection in about 20% of applications, which discourages widespread use among smaller fabricators.

-

Evolving Environmental Regulations: Sectors like marine and industrial coatings grapple with stringent rules on heavy metal content and emissions. Approval processes for new additives can span 12-24 months in key markets such as North America and Europe, delaying market entry. Initiatives like the EU's REACH framework scrutinize potential leachates from additives, introducing compliance costs and uncertainty that can deter innovation, especially for novel organic inhibitors aiming to replace legacy chemicals.

Critical Market Challenges Requiring Innovation

The shift from experimental formulations to large-scale production brings forth substantial obstacles. Scaling up synthesis while preserving efficacy proves tough, with yields dropping to 65-75% at ton-level outputs due to reaction variability. Dispersion issues in complex matrices, such as epoxy resins, often result in aggregation that compromises barrier properties in 25-35% of industrial trials. These issues demand hefty R&D commitments, typically accounting for 10-15% of company revenues, erecting barriers for emerging entrants in a field dominated by established players.

Furthermore, the supply chain for raw materials like rare earth compounds and specialty solvents is prone to disruptions, with price swings of 10-20% yearly influenced by geopolitical factors. Handling and storage of volatile additives add 4-6% to logistics costs compared to standard chemicals, fostering hesitation among bulk buyers in volatile industries like shipping and energy.

Vast Market Opportunities on the Horizon

-

Renewable Energy Infrastructure Expansion: As wind turbines and solar panel frames demand corrosion-resistant metals in harsh offshore settings, additives with multifunctional capabilities—such as UV and salt resistance—offer a breakthrough. These solutions can increase equipment uptime by 30-40%, aligning with the global renewable energy market's projected growth to $1.5 trillion by 2030. Pilot tests in North Sea installations have shown 35-45% reductions in maintenance, positioning anticorrosion additives as enablers for cost-effective green energy deployment.

-

Smart and Self-Healing Coatings Development: Emerging nanotechnology integrations allow additives to release inhibitors on demand, revolutionizing protective systems. In oil rigs and bridges, such technologies extend asset life by 4-7 years, targeting the $20 billion industrial coatings sector. Breakthroughs in microcapsule-based self-healing, achieving 60-75% damage recovery, promise to slash downtime in critical applications, particularly as infrastructure aging becomes a pressing concern worldwide.

-

Collaborative R&D and Supply Chain Alliances: Industry consortia are proliferating, with more than 40 partnerships in the past two years linking additive producers with end-users for tailored solutions. These collaborations shorten development cycles by 25-35%, mitigating risks and fostering innovation in areas like bio-derived inhibitors. By sharing expertise, they bridge gaps in scalability and regulatory navigation, accelerating commercialization in high-stakes fields like defense and transportation.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Solvent-based Preservatives, Water-based Preservatives, and others. Water-based Preservatives currently leads the market, favored for its environmental compliance, lower volatility, and compatibility with modern low-emission coatings used in automotive and construction applications. The solvent-based variants remain crucial for high-solids systems where rapid curing and deep penetration into metal pores are essential.

By Application:

Application segments include Automobile, Aerospace industry, Achitechive, and others. The Automobile segment currently dominates, driven by the need for long-lasting underbody and chassis protections amid rising vehicle production and export demands. However, the Aerospace and Achitechive segments are expected to exhibit the highest growth rates in the coming years, fueled by infrastructure investments and advanced material requirements.

By End-User Industry:

The end-user landscape includes Automobile, Aerospace, Construction, Energy, and Others. The Automobile industry accounts for the major share, leveraging additives for enhanced durability in harsh road conditions and body panels. The Energy and Aerospace sectors are rapidly emerging as key growth end-users, reflecting trends in offshore installations and lightweight aircraft designs that demand superior corrosion mitigation.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/262952/global-metal-anticorrosion-additives-forecast-market-2024-2030-56

Competitive Landscape:

The global Metal Anticorrosion Additives market is semi-consolidated and characterized by intense competition and rapid innovation. The top three companies—Ascotec (France), Lubrizol (U.S.), and BASF (Germany)—collectively command approximately 50% of the market share as of 2023. Their dominance is underpinned by extensive IP portfolios, advanced production capabilities, and established global distribution networks.

List of Key Metal Anticorrosion Additives Companies Profiled:

-

Ascotec (France)

-

Lubrizol (U.S.)

-

BASF (Germany)

-

Ankush Enterprise (India)

-

DOG Deutsche Oelfabrik (Germany)

-

DeVere Chemical (U.K.)

-

Applied Graphene Materials (U.K.)

-

SpecialChem (France)

-

ADDAPT Chemicals (Norway)

-

Advancion (U.S.)

-

Allnex (Belgium)

-

Borchers (U.S.)

The competitive strategy is overwhelmingly focused on R&D to enhance product quality and reduce costs, alongside forming strategic vertical partnerships with end-user companies to co-develop and validate new applications, thereby securing future demand.

Regional Analysis: A Global Footprint with Distinct Leaders

-

North America: Is the undisputed leader, holding a 40% share of the global market. This dominance is fueled by massive R&D investments, a robust chemicals ecosystem, and strong demand from its leading automotive, aerospace, and energy sectors. The U.S. is the primary engine of growth in the region.

-

Europe & China: Together, they form a powerful secondary bloc, accounting for 45% of the market. Europe's strength is driven by strict environmental regulations and innovation in sustainable coatings. China, supported by significant government backing and a massive manufacturing base, is a dominant producer and a rapidly growing consumer, particularly in construction and automotive.

-

Asia-Pacific (ex-China), South America, and MEA: These regions represent the emerging frontier of the Metal Anticorrosion Additives market. While currently smaller in scale, they present significant long-term growth opportunities driven by increasing industrialization, investments in infrastructure and energy, and a growing focus on durable materials.

Get Full Report Here: https://www.24chemicalresearch.com/reports/262952/global-metal-anticorrosion-additives-forecast-market-2024-2030-56

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/262952/global-metal-anticorrosion-additives-forecast-market-2024-2030-56

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/