How Fast Is Data Center Insulation Material Solutions market Growing? Key Trends, Opportunities & Market Outlook

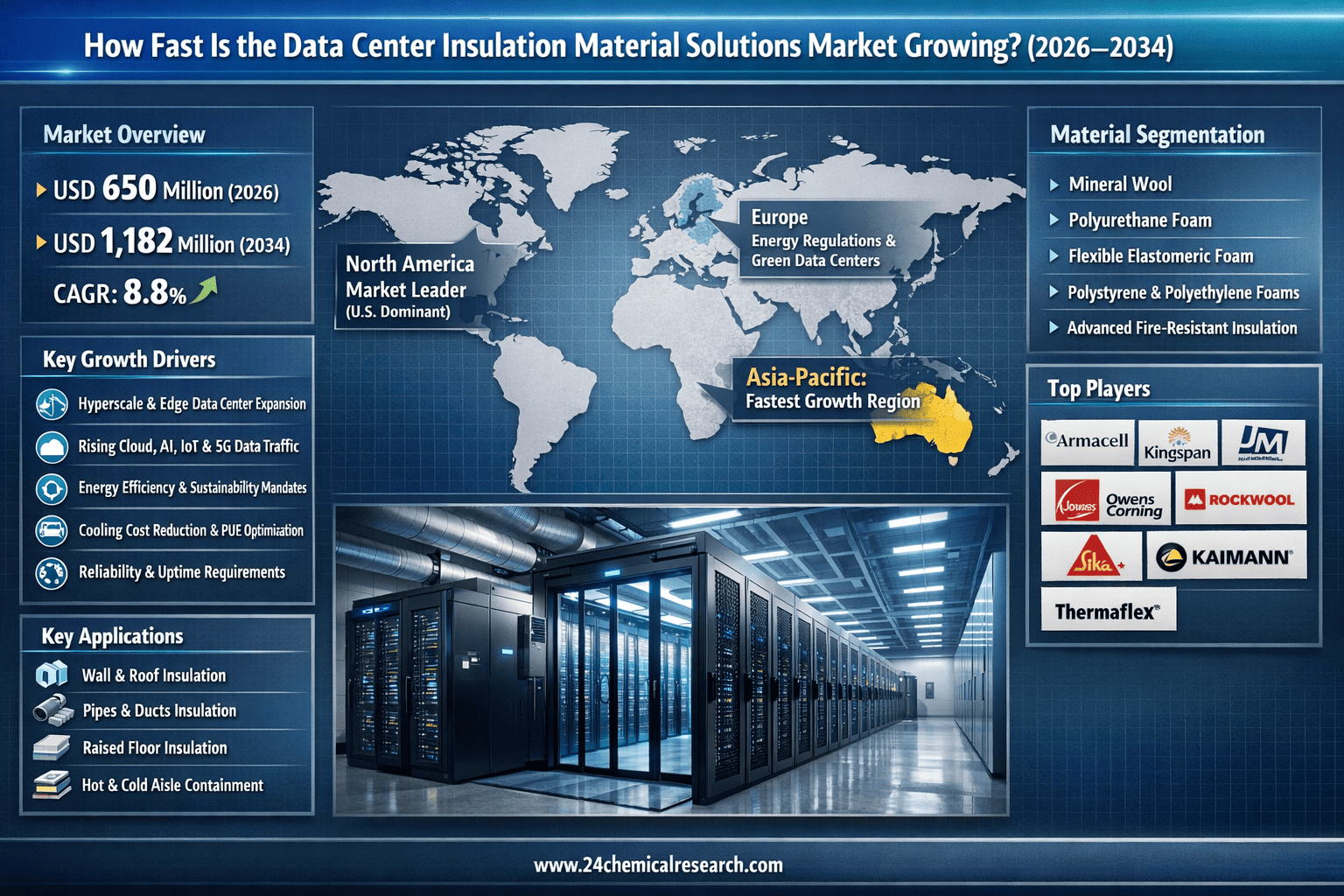

According to 24Chemical Research, Global Data Center Insulation Material Solutions market was valued at USD 650 million in 2026 and is projected to reach USD 1,182 million by 2034, exhibiting a remarkable CAGR of 8.8% during the forecast period.

Data Center Insulation Material Solutions comprise advanced materials and systems specifically engineered to manage the thermal environment within data centers. These solutions include insulation materials like mineral wool, polyurethane foam, and flexible elastomeric foam, alongside fire-resistant and acoustic insulation products. A critical component involves airflow management systems such as hot and cold aisle containment. Their primary function is to minimize heat loss, prevent thermal leakage, maintain stable operating conditions for sensitive IT equipment, and significantly enhance cooling efficiency—directly translating to substantial energy savings and improved operational reliability.

Get Full Report Here: https://www.24chemicalresearch.com/reports/299569/data-center-insulation-material-solutions-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

-

Exponential Growth in Data Generation and Hyperscale Expansion: The relentless surge in data creation, fueled by cloud computing, IoT, AI, and 5G, is fundamentally driving the construction of new hyperscale and edge data centers globally. This expansion creates massive demand for advanced thermal management solutions. Effective insulation is crucial because cooling can account for up to 40% of a data center's total energy consumption. By improving insulation, operators can dramatically enhance Power Usage Effectiveness (PUE), a key metric for efficiency, making it a top priority for new builds and retrofits alike.

-

Stringent Energy Efficiency and Sustainability Mandates: Governments and international bodies are implementing rigorous regulations to reduce energy consumption and carbon emissions. Data centers, as significant energy users, are primary targets. Standards from organizations like ASHRAE and green building certifications like LEED compel operators to invest in superior insulation to minimize energy loss in HVAC systems. The global push towards achieving net-zero emissions is making energy-efficient infrastructure, including high-performance insulation, a non-negotiable aspect of modern data center design and operation.

-

Rising Focus on Operational Expenditure Reduction and Reliability: Beyond regulatory compliance, the rising cost of energy is a powerful economic driver. High-quality insulation directly lowers operational expenditures by reducing the cooling load required to maintain optimal temperatures. This not only improves the bottom line but also enhances the reliability and lifespan of critical IT equipment by preventing thermal stress and moisture-related damage, which are common causes of downtime in poorly insulated facilities.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/299569/data-center-insulation-material-solutions-market

Significant Market Restraints Challenging Adoption

Despite its clear benefits, the market faces hurdles that must be overcome to achieve universal adoption.

-

High Initial Investment and Cost Sensitivity: While insulation delivers significant long-term savings, the upfront capital expenditure for advanced solutions can be substantial. Premium materials like aerogels or specialized elastomeric foams command a higher price compared to traditional options like fiberglass. This high initial cost can be a barrier, particularly for smaller data center operators or in emerging markets where capital budgets are constrained and the focus is often on rapid, low-cost deployment rather than long-term efficiency.

-

Complex Retrofitting and Installation Challenges: Integrating high-performance insulation into existing data centers is often a complex, disruptive, and costly process. Retrofitting requires meticulous planning to avoid service interruptions, and the physical constraints of older facilities can severely limit the options available. This complexity increases labor costs and extends project timelines, posing a significant challenge for operators seeking to upgrade their infrastructure to modern efficiency standards.

Critical Market Challenges Requiring Innovation

The transition from standard practice to optimized, large-scale implementation presents its own set of technical and logistical challenges.

Material performance consistency remains a key hurdle, especially when scaling production to meet the demands of massive hyperscale projects. Furthermore, ensuring that these materials meet the stringent fire safety standards required for environments packed with high-value electrical equipment, such as NFPA codes for low flame spread and smoke development, adds a layer of complexity to product development and selection.

Additionally, the market contends with supply chain dependencies. The production of key insulation materials relies on petrochemical feedstocks and specialized minerals. Volatility in the prices and availability of these raw materials, often influenced by geopolitical and logistical factors, can lead to cost fluctuations and supply instability, creating economic uncertainty for both manufacturers and end-users planning large-scale deployments.

Vast Market Opportunities on the Horizon

-

Innovation in Sustainable and High-Performance Materials: There is a significant opportunity for the development and commercialization of next-generation insulation materials. Bio-based foams, materials with high recycled content, and advanced aerogels offer the potential for even greater thermal resistance (higher R-values) with a substantially reduced environmental footprint. As data center operators face increasing pressure to meet ambitious sustainability targets, the demand for these innovative, eco-friendly solutions that do not compromise on performance or safety is expected to create substantial new market avenues.

-

Expansion of Edge Computing and Modular Data Centers: The rapid deployment of edge computing facilities and modular data centers presents a robust and distinct growth vector. Unlike traditional large-scale facilities, edge data centers are often located in non-traditional, space-constrained, or harsh environments. This creates a specific need for compact, durable, easy-to-install, and highly efficient insulation solutions tailored to these unique challenges, opening up new and specialized application niches for innovative material providers.

-

Advanced Fire Protection and Acoustic Management Integration: Beyond thermal management, there is growing recognition of the need for integrated solutions. Insulation that provides superior fire resistance—a critical safety requirement—as well as effective acoustic damping to reduce noise from cooling systems represents a significant value-added opportunity. The development of multi-functional materials that address thermal, fire, and acoustic needs simultaneously is poised to become a key differentiator and growth area in the market.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Material Type:

The market is segmented into Mineral Wool, Polyurethane Foam, Polyethylene Foam, Polystyrene Foam, Flexible Elastomeric Foam, and others. Mineral Wool is widely considered a leading segment due to its superior inherent fire resistance and excellent acoustic damping properties, making it a fundamental choice for ensuring overall facility safety and stability. Meanwhile, Flexible Elastomeric Foam is gaining significant traction for its exceptional thermal performance, moisture resistance, and ease of installation on complex piping systems, which is critical for preventing condensation and managing chilled water lines.

By Application:

Application segments include Wall & Roof Insulation, Raised Floor Insulation, Pipes & Ducts Insulation, and others. The Pipes & Ducts application is paramount as it is integral to the efficiency of the entire cooling system, which constitutes the largest portion of a data center's energy draw. Effective insulation on chilled water pipes and air-handling ductwork is crucial for minimizing thermal loss. Simultaneously, Raised Floors remain a critical application for facilities using underfloor air distribution, where insulation contributes to thermal management, structural integrity, and fire compartmentalization.

By End-User Industry:

The end-user landscape is primarily divided into Hyperscale Data Centers, Enterprise Data Centers, and Edge Data Centers. Hyperscale Data Centers dominate demand due to their enormous scale, continuous global expansion, and extreme focus on achieving the lowest possible PUE, creating a concentrated need for high-performance, scalable insulation solutions. The rapidly growing Edge Data Center segment represents a key growth area, demanding specialized solutions for decentralized, often unconventional locations.

Get Full Report Here: https://www.24chemicalresearch.com/reports/299569/data-center-insulation-material-solutions-market

Download FREE Sample Report:

List of Key Data Center Insulation Material Solutions Companies Profiled

-

Armacell (Germany)

-

Kingspan Group (Ireland)

-

Johns Manville (United States)

-

Kaimann (Germany)

-

Owens Corning (United States)

-

Boyd (United States)

-

The Supreme Industries Ltd. (India)

-

Sika Ag (Switzerland)

-

Ventac (Ireland)

-

Rockwool A/S (Denmark)

-

Thermaflex (Netherlands)

Data Center Insulation Material Solutions Market Trends

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch